Tomorrow officially marks the new year. That means the big-boys look more and more at 2011 estimates. For large multi-national corporations (ie IBM, GS, MSFT, INTC, AAPL, F etc) earnings estimates will be strong.

Let me use IBM as an example (but each company has their own specific situation regarding product cycles and macro economic effects)...

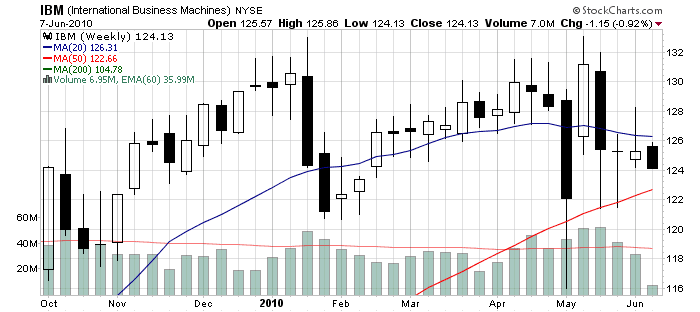

The longer-term:

With today's move, IBM is trading with a trailing PE of 12, and 2011 forward est. PE is at 10.1. Their CEO was very clear discussing their expected $20eps earnings by 2015 due to their business and backlog. The CEO did this before, and IBM exceeded the previous projections. IBM has a history of over-delivering. (This was with the greatest recession of our life time.) So a forward PE of 10.1, with a company of this track record, means IBM is very cheap here.

The shorter-term:

Over the last couple of months IBM has been trading with a PE around 12. Currently IBM is projected to complete the 2010 year with an eps of 11.27, but when taking into account its consistent out performance, it should be more like 11.50. Slap a 12 PE on these figure we have a stock that should have a trailing PE of 135-138 by the end of this year.

The market attempts to predict. It will begin to price in 2011 earnings in the second half of the year because that is how the big-boys play this game (when they are not sucking their thumbs :). If the stock does not begin to price it in, the street will be saying that eps will decline. Considering the history of management, and the product cycle the sector is in (and the fact that corporations are not slowing down IT spending despite a threat of double-dip recession because companies have the largest amount of cash on their balance sheet is 30 some years), the market will be wrong.

Corporate spending on certain things will be maintained no matter the environment. Another 'Lehman-freeze in credit' will not happen, at least over the next 3 years. There is too much liquidity available via the $1 trillion dollar Euro deal, approximately 50% of the American stimulus needing to be spent and Asia still doing okay.

We may slow down some, but markets will not freeze. The example above with IBM can be done with pretty much all the multi-nationals. Because of this, in my opinion, the anticipated slow down is priced into the market right now. And it is creating inefficiencies in prices for names like IBM. (Any many many others like F, MSFT, INTC etc.)

Wednesday, June 30, 2010

uhm... yeah

I don't know what to make of this.

I do know, I am looking at individual names, and am not backing away from IBM. (I added just now.)

GS is approaching book value. Reports of 122 are floating around, but Yahoo Finance has it pegged at 128. Basically the market is selling GS with little-to-no future earnings potential.

C it is a steal right now.

Other names I can be patient on until the big boys stop sucking their thumbs.

I do know, I am looking at individual names, and am not backing away from IBM. (I added just now.)

GS is approaching book value. Reports of 122 are floating around, but Yahoo Finance has it pegged at 128. Basically the market is selling GS with little-to-no future earnings potential.

C it is a steal right now.

Other names I can be patient on until the big boys stop sucking their thumbs.

Tuesday, June 29, 2010

Market Thought... da bears

I had to limit my media intake this evening. There is simply too much negativity. Everyone is singing the same tune, and all the big-boys appear to be curled up in the fetal position. Although I will give it to Cramer to try to lighten the mood, he is not without his caveats.

The information we got today was negative, the charts are now obviously negative, and the one-sided mentality is confirmed from the broad media reports I am seeing.

But, how can we possible be as negative as everyone else when we knew this was coming? We saw this coming via the recent Market Thought posts 'a hint of concern' to 'think ahead'. As for me, I just can not be.

I have not posted this chart in some time, however the 1040 level is a strong support level. The strength comes from the current trading dynamic with the 1040 level being the low end of an apparent channel. But, it also is a support of a larger macro support, that appears very favorable.

The chart is a 10 year look at the 320 SMA. It has consistently been a major support/resistance point for OVER 10 years. I only included the 10 years so that the point is visible. (There was a period in 1994-1995 where the support did not hold, and the SP500 simply channel traded for a year.)

The chart is a 10 year look at the 320 SMA. It has consistently been a major support/resistance point for OVER 10 years. I only included the 10 years so that the point is visible. (There was a period in 1994-1995 where the support did not hold, and the SP500 simply channel traded for a year.)

Ultimately we are all held hostage to Mr. Market, and we little people can only try to take advantage. The SP500 is down 9-10%, since hitting 1130, within a 7 day period. (That is pretty fast.)

All I can control is what I do, and with this decline, I went from approximately 60% cash to about less than 20%.

(Keep in mind when it was around 60, it was much higher because I do short, while being long certain positions, and constantly churn the portfolio. Also, less than 20% is very very low for me due to the option strategies that I invoke.)

The information we got today was negative, the charts are now obviously negative, and the one-sided mentality is confirmed from the broad media reports I am seeing.

But, how can we possible be as negative as everyone else when we knew this was coming? We saw this coming via the recent Market Thought posts 'a hint of concern' to 'think ahead'. As for me, I just can not be.

I have not posted this chart in some time, however the 1040 level is a strong support level. The strength comes from the current trading dynamic with the 1040 level being the low end of an apparent channel. But, it also is a support of a larger macro support, that appears very favorable.

The chart is a 10 year look at the 320 SMA. It has consistently been a major support/resistance point for OVER 10 years. I only included the 10 years so that the point is visible. (There was a period in 1994-1995 where the support did not hold, and the SP500 simply channel traded for a year.)

The chart is a 10 year look at the 320 SMA. It has consistently been a major support/resistance point for OVER 10 years. I only included the 10 years so that the point is visible. (There was a period in 1994-1995 where the support did not hold, and the SP500 simply channel traded for a year.)Ultimately we are all held hostage to Mr. Market, and we little people can only try to take advantage. The SP500 is down 9-10%, since hitting 1130, within a 7 day period. (That is pretty fast.)

All I can control is what I do, and with this decline, I went from approximately 60% cash to about less than 20%.

(Keep in mind when it was around 60, it was much higher because I do short, while being long certain positions, and constantly churn the portfolio. Also, less than 20% is very very low for me due to the option strategies that I invoke.)

Summary of Today Catalysts

Andrew Busch gave a nice summary of today's market catalysts. In turn, these events are causing the 'risk-off' theme to play out.

I get this concept of 'risk-off' when the market is much higher, but right now, with companies trading at already depressed multiples and treasury yields so low, the 'risk-off' theme makes little sense to me.

(Thought the article summed everything up nicely, so I wanted to share it and save the link.)

I get this concept of 'risk-off' when the market is much higher, but right now, with companies trading at already depressed multiples and treasury yields so low, the 'risk-off' theme makes little sense to me.

(Thought the article summed everything up nicely, so I wanted to share it and save the link.)

trades...

1. Covered my protection.

2. Bought an initial position of F at 9.90.

The market may decline to the 320 SMA support, but I want a quick finger when AAPL reaches 253. Also, I will buy more NAT and IBM when the SP500 approaches 1045. (I already own the names at/below current levels, I would like to get them lower. Although I question whether or not IBM will break 127.)

2. Bought an initial position of F at 9.90.

The market may decline to the 320 SMA support, but I want a quick finger when AAPL reaches 253. Also, I will buy more NAT and IBM when the SP500 approaches 1045. (I already own the names at/below current levels, I would like to get them lower. Although I question whether or not IBM will break 127.)

Monday, June 28, 2010

Market Thought... waiting

My short-term thesis has not changed from the previous Market Thought post 'think ahead'. The thesis is playing out, with the 10yr yield approaching 3.0, although the treasuries are very overbought (meaning the bonds need to sell off, raising the yield), and the SP500 has declined some and is oversold.

Since last week, the market churn has allowed the 320SMA to achieve 1041-1042. This means there is a fairly sizable support level at the 1040 level.

The names I will be looking to get in, as the markets decline to the 1040 level have not changed.

The names I will be looking to get in, as the markets decline to the 1040 level have not changed.

Since I already to C the other day, and already pretty long GS, I want to continue adding to IBM (although already my largest position) and NAT.

ON A SIDE NOTE: Read an article today regarding freight container shortages. Thought it was interesting because the BDI does not correlate to the article. I would expect to see the BDI higher due to this shortage. Will keep my eye on this trend, but a container shortage is a fairly bullish development.

Since last week, the market churn has allowed the 320SMA to achieve 1041-1042. This means there is a fairly sizable support level at the 1040 level.

The names I will be looking to get in, as the markets decline to the 1040 level have not changed.

The names I will be looking to get in, as the markets decline to the 1040 level have not changed.Since I already to C the other day, and already pretty long GS, I want to continue adding to IBM (although already my largest position) and NAT.

ON A SIDE NOTE: Read an article today regarding freight container shortages. Thought it was interesting because the BDI does not correlate to the article. I would expect to see the BDI higher due to this shortage. Will keep my eye on this trend, but a container shortage is a fairly bullish development.

Sunday, June 27, 2010

lighting up GS

Over the next few days, buy/sell signals will be flashing for the Goldman. The chart set up is very interesting, and the next few days will be telling.

The negative trend, and lifeless lingering, of the last two months looks to be breaking.

The negative trend, and lifeless lingering, of the last two months looks to be breaking.

Its no surprise that I have been bullish on the name. Now that FinReg is completed and certainty creeping into the minds of traders, the set up may lead GS to test the high 150s.

I will look to sell around 156, as per the weekly, this is the first SMA resistance.

(Although, if feeling very aggressive, the upper range of 170ish is a possibility.)

(Although, if feeling very aggressive, the upper range of 170ish is a possibility.)

The negative trend, and lifeless lingering, of the last two months looks to be breaking.

The negative trend, and lifeless lingering, of the last two months looks to be breaking.Its no surprise that I have been bullish on the name. Now that FinReg is completed and certainty creeping into the minds of traders, the set up may lead GS to test the high 150s.

I will look to sell around 156, as per the weekly, this is the first SMA resistance.

(Although, if feeling very aggressive, the upper range of 170ish is a possibility.)

(Although, if feeling very aggressive, the upper range of 170ish is a possibility.)

NatGas drilling the GasLand

Over the weekend I saw the new documentary GasLand. I have to say, I was glued to the TV. The kind of documented proof regarding the hazards of Nat. Gas drilling are difficult to dispute, but the industry is trying. They created EnergyInDepth.org to try to explain away, and discredit Josh Fox as a sensationalist. After reading the site, I have to say, ultimately the site is simply fluff.

When the fluff is stripped away, the argument boils down to the fact that "massive" pollution is not occurring. But that is only because Nat Gas drilling is not yet taking place in heavily populated areas.

I am a fan of using Natural Gas. I really am. But I just so happen to be an engineer that manages manufacturing discrepancies within THE MOST regulated industry (the Pharma/Biotech industry). Been doing so for 8 years, and understand when something is not regulated enough and when something is too regulated. The Nat. Gas drillers and distributors are not regulated enough.

The tangible evidence presented in this documentary blatantly shows the Natural Gas drillers are clearly not regulated enough. There is an extreme lack of safety, health and environmental standards.

The current state of the industry can not exist in its current form. There is simply too much health risk in densely populated areas. The industry will be forced to adapt just like the food industry changed when The Jungle was published.

(a PBS interview with Josh Fox)

When the fluff is stripped away, the argument boils down to the fact that "massive" pollution is not occurring. But that is only because Nat Gas drilling is not yet taking place in heavily populated areas.

I am a fan of using Natural Gas. I really am. But I just so happen to be an engineer that manages manufacturing discrepancies within THE MOST regulated industry (the Pharma/Biotech industry). Been doing so for 8 years, and understand when something is not regulated enough and when something is too regulated. The Nat. Gas drillers and distributors are not regulated enough.

The tangible evidence presented in this documentary blatantly shows the Natural Gas drillers are clearly not regulated enough. There is an extreme lack of safety, health and environmental standards.

The current state of the industry can not exist in its current form. There is simply too much health risk in densely populated areas. The industry will be forced to adapt just like the food industry changed when The Jungle was published.

(a PBS interview with Josh Fox)

Thursday, June 24, 2010

A word on BP

I owned (past tense) BP to trade around its asset value. 29 was broken today. It may bounce off this level, it may collapse I do not know. (I am still letting the Jan 2011 $10 strike puts ride.)

The one thing I do know is that when comparing risk trades at current levels C, GS, IBM, F, MF and many other names have a far better risk/reward profile compared to BP at the moment.

Because of this, and the breach of the 29 support, I sold the BP common and added to C and IBM today.

The one thing I do know is that when comparing risk trades at current levels C, GS, IBM, F, MF and many other names have a far better risk/reward profile compared to BP at the moment.

Because of this, and the breach of the 29 support, I sold the BP common and added to C and IBM today.

frustrating!!!

I set up my trading capability quite nicely with respect to having a job that is completely not related to trading. But ever since my company got bought out by Pfizer, their IT monitoring system only allows certain 'activity-per-few-minutes' of use. (Despite the fact they let us use Facebook!)

Since I have my screens up all the time, and the way Yahoo Finance ads work, it constantly shuts me out of the Internet.

I was always able to work around it, but today it is frustrating me to no end.

At this point, I want to take a package, and trade full time with the proper high-frequency trading tools.

Since I have my screens up all the time, and the way Yahoo Finance ads work, it constantly shuts me out of the Internet.

I was always able to work around it, but today it is frustrating me to no end.

At this point, I want to take a package, and trade full time with the proper high-frequency trading tools.

Wednesday, June 23, 2010

Market Thought... think ahead

We are just in a sea of negativity. The Fed. statement was no different. In my opinion, it corroborated what we are seeing in the 10yr treasury yield.

The yield is currently hitting its high-end support. It looks to want to test the low-end (3.0).

If it does, do not fear it. The fear of deflation will take the market down with it.

If it does, do not fear it. The fear of deflation will take the market down with it.

An important event took place after I published my Market Thought post 'hint of concern'. China indicated they will begin revaluing the Yuan. We may have seen hints of this in the 5yr treasury market with the relative weak demand. The Yuan/dollar adjustment would mean higher inflation, and higher rates.

This is why, fundamentally speaking (in pure economic algebra), the 10yr treasury yield will not break 3.0 to merit real deflationary concern. But since the 'hint of concern' post, I did see a few interviews highlighting this as a concern, so I must assume its baked into the hedgies at this point. When/if the current support is broken, it may trigger a market sell off that may lead the SP500 to its daily 320SMA.

We may see a new level of fear, capitulating the market and present a buying opportunity.

We may see a new level of fear, capitulating the market and present a buying opportunity.

I will look to add IBM (calls), AAPL (calls), F (common), GS (calls), NAT (common), C (common) and JCG (common).

Around the 1040 level of the SP500, valuations matter. The street will price in deflation, but as mentioned above, they will be wrong.

The yield is currently hitting its high-end support. It looks to want to test the low-end (3.0).

If it does, do not fear it. The fear of deflation will take the market down with it.

If it does, do not fear it. The fear of deflation will take the market down with it.An important event took place after I published my Market Thought post 'hint of concern'. China indicated they will begin revaluing the Yuan. We may have seen hints of this in the 5yr treasury market with the relative weak demand. The Yuan/dollar adjustment would mean higher inflation, and higher rates.

This is why, fundamentally speaking (in pure economic algebra), the 10yr treasury yield will not break 3.0 to merit real deflationary concern. But since the 'hint of concern' post, I did see a few interviews highlighting this as a concern, so I must assume its baked into the hedgies at this point. When/if the current support is broken, it may trigger a market sell off that may lead the SP500 to its daily 320SMA.

We may see a new level of fear, capitulating the market and present a buying opportunity.

We may see a new level of fear, capitulating the market and present a buying opportunity.I will look to add IBM (calls), AAPL (calls), F (common), GS (calls), NAT (common), C (common) and JCG (common).

Around the 1040 level of the SP500, valuations matter. The street will price in deflation, but as mentioned above, they will be wrong.

Trades - JCG, MF

Observing an underlining strength, but choppiness remains. Regardless, I see value in JCG and MF.

I also see value in GS today, and will probably add to the my position.

I also see value in GS today, and will probably add to the my position.

Tuesday, June 22, 2010

Is the SEC f-ing kidding?!?

While reading this article/interview with Robert Khuzami, SEC director of enforcement, he specifically states:

"It’s no defense to claim that your client was a sophisticated investor"

Is he fucking shitting all of us? We pay tax dollars to support an organization that has allowed ponzi scheme after ponzi scheme plunder the unsophisticated investor for YEARS!!! Their actions were so negligent that I would argue the SEC were criminal, and the SEC themselves should be sued by the victims.

Just because someone is wealthy, by monetary standards, does not mean they are sophisticated investors. I can name plenty of people who fit that bill. BUT, individuals that work for banks, have industry standard certifications and know very well what type of market they are dealing with, are sophisticated. The SEC has no business protecting these people.

If these sophisticated investors do not like a market, don't trade it. They are uncomfortable with the transparency of a piece of paper, demand clarity or do not trade it.

I do not want my tax dollars being spent on protecting 'sophisticated' investors crying foul when they make a STUPID FUCKING DECISION! Its a moral hazard, and dumb-ass Khuzami is promoting the moral hazard with his statement above.

The SEC better wake up.

"It’s no defense to claim that your client was a sophisticated investor"

Is he fucking shitting all of us? We pay tax dollars to support an organization that has allowed ponzi scheme after ponzi scheme plunder the unsophisticated investor for YEARS!!! Their actions were so negligent that I would argue the SEC were criminal, and the SEC themselves should be sued by the victims.

Just because someone is wealthy, by monetary standards, does not mean they are sophisticated investors. I can name plenty of people who fit that bill. BUT, individuals that work for banks, have industry standard certifications and know very well what type of market they are dealing with, are sophisticated. The SEC has no business protecting these people.

If these sophisticated investors do not like a market, don't trade it. They are uncomfortable with the transparency of a piece of paper, demand clarity or do not trade it.

I do not want my tax dollars being spent on protecting 'sophisticated' investors crying foul when they make a STUPID FUCKING DECISION! Its a moral hazard, and dumb-ass Khuzami is promoting the moral hazard with his statement above.

The SEC better wake up.

Monday, June 21, 2010

Action on BP

BP has real assets, pegged to real commodities. At the moment the stock is trading around its book value. If I were to believe Yahoo Finance, it is trading approximately 9% below book value.

Due to the liability uncertainty I believe the stock will trade around book value, buying the stock when BP is below it and selling the stock when BP is above it.

The other day I realized that if BP begins to trade too much below book value, the market is either being extremely inefficient or predictive. I have come to the conclusion, if the 29 support level is broken, the divergence between book value and stock price will indicate the market will be predicting.

So, as a fixed cost hedge, I purchased a few Jan 2011 puts (with $10 strike). I have no concern to completely lose this amount of cash as the options are around $0.60. I believe I will more than cover this cost trading BP, and if 28.50 is breached on BP I will sell the stock and let the options simply ride.

(PS... The CEO attending the Yacht race over the weekend merits a complete termination from the company. For a man so in love with the sea, I am shocked he is not pushing his company to do more to clean up as the spill is taking place. The man is either too stupid or too apathetic. He should be fired.)

Due to the liability uncertainty I believe the stock will trade around book value, buying the stock when BP is below it and selling the stock when BP is above it.

The other day I realized that if BP begins to trade too much below book value, the market is either being extremely inefficient or predictive. I have come to the conclusion, if the 29 support level is broken, the divergence between book value and stock price will indicate the market will be predicting.

So, as a fixed cost hedge, I purchased a few Jan 2011 puts (with $10 strike). I have no concern to completely lose this amount of cash as the options are around $0.60. I believe I will more than cover this cost trading BP, and if 28.50 is breached on BP I will sell the stock and let the options simply ride.

(PS... The CEO attending the Yacht race over the weekend merits a complete termination from the company. For a man so in love with the sea, I am shocked he is not pushing his company to do more to clean up as the spill is taking place. The man is either too stupid or too apathetic. He should be fired.)

Sunday, June 20, 2010

Market Thought... a hint of concern

Before I begin... Happy Father's Day.

I noticed a subtle set-up that may hint toward an indication of concern. The SP 500 is up nicely since the 1040/1050 level, but when it is correlated against the 10yr treasury yield I get the feeling the yield should be higher.

I will not post charts because the set-up is particularly subtle, and easily arguable. It may very well lead to nothing, but the seed of doubt regarding strong GDP growth comes to mind.

I am keeping a close eye on the 10yr treasury yield as a break of the 3.0-3.1 level will indicate deflation, and a weak equity market.

The markets are overbought, and a declining market usually correlates to a declining treasury yield. This subtle set-up may lead to the 'deflationary' support level being tested, hence my concern.

If the yield rallies from here or off the 3.1-3.2 level, upon a market pull back, this concern will mitigate.

This post is just a heads up, as the set-up may lead to a change in market thesis.

I noticed a subtle set-up that may hint toward an indication of concern. The SP 500 is up nicely since the 1040/1050 level, but when it is correlated against the 10yr treasury yield I get the feeling the yield should be higher.

I will not post charts because the set-up is particularly subtle, and easily arguable. It may very well lead to nothing, but the seed of doubt regarding strong GDP growth comes to mind.

I am keeping a close eye on the 10yr treasury yield as a break of the 3.0-3.1 level will indicate deflation, and a weak equity market.

The markets are overbought, and a declining market usually correlates to a declining treasury yield. This subtle set-up may lead to the 'deflationary' support level being tested, hence my concern.

If the yield rallies from here or off the 3.1-3.2 level, upon a market pull back, this concern will mitigate.

This post is just a heads up, as the set-up may lead to a change in market thesis.

Friday, June 18, 2010

birthday gift

Cheers to another year young... happy birthday to me :)

Today an interesting set up regarding JPM developed. It is breaking from its negative trend. IMO, this is a good indicator to the broader financial sector.

The 20SMA was clearly a resistance point, and today if this set-up holds, JPM will no longer be in that down-trend.

The 20SMA was clearly a resistance point, and today if this set-up holds, JPM will no longer be in that down-trend.

JPM looks to be a buy right now, and the next level of resistance is around high 40-low 41.

(I am playing the anticipated push up within financials via GS and C, and am using JPM as an indicator.)

Today an interesting set up regarding JPM developed. It is breaking from its negative trend. IMO, this is a good indicator to the broader financial sector.

The 20SMA was clearly a resistance point, and today if this set-up holds, JPM will no longer be in that down-trend.

The 20SMA was clearly a resistance point, and today if this set-up holds, JPM will no longer be in that down-trend. JPM looks to be a buy right now, and the next level of resistance is around high 40-low 41.

(I am playing the anticipated push up within financials via GS and C, and am using JPM as an indicator.)

Thursday, June 17, 2010

Market Thought... trading dynamic

To say the market should be going much lower, then state AAPL and other big tech companies (including INTC, IBM, ect.) are inexpensive is a contradiction.

There is always a potential reason as to why the markets move the way they do. The reality of trading is that markets, in the short-term, are inefficient, especially when uncertainty presents itself. But longer-term, tend to be efficient. The trick is to take advantage of the short-term inefficiency to benefit from the long-term efficiency.

Whatever the reasons the gurus want to give as to why the tape acted the way it did, their explanation is irrelevant. Markets have always (ALWAYS) traded via patterns (ie charts) and fundamentals.

Charts can peek into the mob mentality of the market. Chart not only give an investor trading reference points, it allows an investor to predict fears. (While not easy to do, tt gives a human investor a benefit over the algorithm trading machine. Machines follow patterns, there is no uncertain element within their program. Human traders are trickier in that they do have an uncertain element, emotion.)

Fundamentals are ultimately what drives long-term efficiency. Valuations do matter, and valuations are currently below there norm.

So when someone is asking why didn't the market collapse today, I say 'why should it collapse?'

1. Perceived negativity in the Euro zone is declining. The fact that the euro is up, imo is nothing more than seasonality. (I have been going to Europe for more than 15years in the summer time, and through all those years I can say with utter certainty the country's currency at the time always appreciated during the summer months, at least when I was there. It would piss me off to exchange at a higher rate then the week before, so much so that its etched in my memory :).

2. Valuations are very inexpensive, even when considering earnings estimate cuts.

Regardless, the SP500 can retest the 1050 level, as we are in uncertain territory here. But when clarity develops, the big-boys will grow a pair, volumes will increase and legitimize the market moves. Until then, day-traders, the high frequency algorithms and then few bottom feeders control the tape.

There is always a potential reason as to why the markets move the way they do. The reality of trading is that markets, in the short-term, are inefficient, especially when uncertainty presents itself. But longer-term, tend to be efficient. The trick is to take advantage of the short-term inefficiency to benefit from the long-term efficiency.

Whatever the reasons the gurus want to give as to why the tape acted the way it did, their explanation is irrelevant. Markets have always (ALWAYS) traded via patterns (ie charts) and fundamentals.

Charts can peek into the mob mentality of the market. Chart not only give an investor trading reference points, it allows an investor to predict fears. (While not easy to do, tt gives a human investor a benefit over the algorithm trading machine. Machines follow patterns, there is no uncertain element within their program. Human traders are trickier in that they do have an uncertain element, emotion.)

Fundamentals are ultimately what drives long-term efficiency. Valuations do matter, and valuations are currently below there norm.

So when someone is asking why didn't the market collapse today, I say 'why should it collapse?'

1. Perceived negativity in the Euro zone is declining. The fact that the euro is up, imo is nothing more than seasonality. (I have been going to Europe for more than 15years in the summer time, and through all those years I can say with utter certainty the country's currency at the time always appreciated during the summer months, at least when I was there. It would piss me off to exchange at a higher rate then the week before, so much so that its etched in my memory :).

2. Valuations are very inexpensive, even when considering earnings estimate cuts.

Regardless, the SP500 can retest the 1050 level, as we are in uncertain territory here. But when clarity develops, the big-boys will grow a pair, volumes will increase and legitimize the market moves. Until then, day-traders, the high frequency algorithms and then few bottom feeders control the tape.

Wednesday, June 16, 2010

BP = foot-in-mouth

These guys are just stupid at PR, really. The countless video and statement fuck-ups that the CEO and now Chairman are doing are just stupid.

These idiots need to hire the best AMERICAN public relation firm to coach them on public speaking toward Americans, and the adjectives they use.

In this article BP chairman states, "I hear comments sometimes that large oil companies are -- are greedy companies or don't care, but that is not the case in BP. We care about the small people." (i added the bold)

I am sure shit like this does not fly in Britain either, but definitely not in the states.

I just shook my head in amazement when I read that. What fucking idiots.

Update: I just saw the video regarding his statement of "small people", and I must say, it was a translation issue as the comment was an improve answer to a question. I do not think he meant to project an inherent belittling personality of a chairman's superiority amongst the average man. After all, he is Swiss, I think kindness is assimilating within their culture :)

These idiots need to hire the best AMERICAN public relation firm to coach them on public speaking toward Americans, and the adjectives they use.

In this article BP chairman states, "I hear comments sometimes that large oil companies are -- are greedy companies or don't care, but that is not the case in BP. We care about the small people." (i added the bold)

I am sure shit like this does not fly in Britain either, but definitely not in the states.

I just shook my head in amazement when I read that. What fucking idiots.

Update: I just saw the video regarding his statement of "small people", and I must say, it was a translation issue as the comment was an improve answer to a question. I do not think he meant to project an inherent belittling personality of a chairman's superiority amongst the average man. After all, he is Swiss, I think kindness is assimilating within their culture :)

BP looks very interesting intraday

The intraday action (like right now, 11:58am) looks really really interesting. Something is going on triggering heavy positive action and volume.

If it can close up today, I think we have a bottom.

Once I saw the intraday ticker acting this way, I bought it.

If it can close up today, I think we have a bottom.

Once I saw the intraday ticker acting this way, I bought it.

Tuesday, June 15, 2010

Market Thought... oh well

So much for that short-term market consolidation :)

The SP500 closed above its 200 SMA, and across the board the sense that this move up is due to the high frequency folks, end of quarter window dressing and/or any other reason people can think of. (Cramer does a good job summing up these points. However, I do not agree with him or the others.)

The markets are still in a sea-of-resistance. But what looks to be happening right now is the market acting ahead of the FinReg bill, and this is allowing the markets to move up. I linked a video yesterday where FinReg will not be as bad as the market is projecting. The outcome will simply boil down to be forced capital requirements to the trading arm of a bank. This is common sense regulation, and I truly believe its market friendly. This appears to be indicated in the weekly XLF chart, bouncing off of its support line and potentially regaining its 50 SMA support.

This set up should be good for bank stocks (especially GS), and if the market wants to follow them, the market will follow. BUT the market resistance is very real on the daily and weekly charts.

This set up should be good for bank stocks (especially GS), and if the market wants to follow them, the market will follow. BUT the market resistance is very real on the daily and weekly charts.

Whatever the markets decide to do, there are plenty of 'potential-resistance' points, via the technicals, the market can use to begin its consolidation.

The SP500 closed above its 200 SMA, and across the board the sense that this move up is due to the high frequency folks, end of quarter window dressing and/or any other reason people can think of. (Cramer does a good job summing up these points. However, I do not agree with him or the others.)

The markets are still in a sea-of-resistance. But what looks to be happening right now is the market acting ahead of the FinReg bill, and this is allowing the markets to move up. I linked a video yesterday where FinReg will not be as bad as the market is projecting. The outcome will simply boil down to be forced capital requirements to the trading arm of a bank. This is common sense regulation, and I truly believe its market friendly. This appears to be indicated in the weekly XLF chart, bouncing off of its support line and potentially regaining its 50 SMA support.

This set up should be good for bank stocks (especially GS), and if the market wants to follow them, the market will follow. BUT the market resistance is very real on the daily and weekly charts.

This set up should be good for bank stocks (especially GS), and if the market wants to follow them, the market will follow. BUT the market resistance is very real on the daily and weekly charts.

Whatever the markets decide to do, there are plenty of 'potential-resistance' points, via the technicals, the market can use to begin its consolidation.

Monday, June 14, 2010

Market Thought... wall of resistance

I see a relatively healthy market trading on pure technicals. Today's market close or intraday action did not suggest anything out of the ordinary, considering the SP500's technical position.

The SP500 rallied near the 200 SMA and hit the 28 SMA, as one would expect from breaking its previous resistance (the 14SMA). This seems to be trading in a very text-book charting fashion.

The market may come in some, until FinReg is finalized, but after the next consolidation, the 200 SMA may break. (I would not be surprised to consolidate to the 1040-1050 level.)

Also, listening to the accommodating video on CNBC.com w/Volker, I come to the full realization that the 'volker rule' or the separation of swaps to the banks is nothing more than proper capital requirements for the specific trading unit of the bank. Something I completely agree with, and something Goldman Sach already does. (To which I continue to scratch my head as to why it is being punished so much. But I do not think the latter part is completely understood yet.)

The SP500 rallied near the 200 SMA and hit the 28 SMA, as one would expect from breaking its previous resistance (the 14SMA). This seems to be trading in a very text-book charting fashion.

The market may come in some, until FinReg is finalized, but after the next consolidation, the 200 SMA may break. (I would not be surprised to consolidate to the 1040-1050 level.)

Also, listening to the accommodating video on CNBC.com w/Volker, I come to the full realization that the 'volker rule' or the separation of swaps to the banks is nothing more than proper capital requirements for the specific trading unit of the bank. Something I completely agree with, and something Goldman Sach already does. (To which I continue to scratch my head as to why it is being punished so much. But I do not think the latter part is completely understood yet.)

Thoughts on BP

Since everyone and their mother gave their input onto this name, I might as well do so too :). To imagine the worst case scenario, just use your imagination. But certain facts can not be ignored:

1. With a suspended dividend, BP's cash flow alone can handle potential clean up.

2. BP has a book value of mid 33, as per YahooFinance. (In an era of expensive oil, the current level is awfully enticing. Book value depicted as the yellow line in the daily chart below.)

3. One of the best, and level-headed, value investor of our era (Whiteny Tilson) is buying it.

4. The charts look to have begun a stabilization, although it does not look pretty.

29 appears to be a good area, or at least anywhere below the book value (yellow line).

It maybe range bound for sometime between the 29-37 range until more certainty develops around the issue.

Right now there are a lot of possible outcomes, but the least probable is BP going under where shareholders lose total value.

I sold some portfolio (option) positions in this rally, increasing my cash and reducing my leverage, that will allow me to play BP. (Had too much levered risk in the portfolio via various call options so I resisted purchasing BP at 29 last week. Discipline's a bitch.) Will look to actively trade the common around BP's book value for now, purchasing around 29 and selling it after a reasonable increase.

(For the risk adverse trader, a stop around low 28 would not be a bad idea. But I do not use stops.)

Saturday, June 12, 2010

Trade - GS

I listen to the linked video and I hear a level headed group of leaders, regardless of the nitpicking. (FinReg showdown)

I see the decline of GS over the past few weeks, and think it is very over stated. With the bill coming through over the next few weeks, reported earnings coming due and the fact that GS is trading very close to book value, I am expecting GS bounce and hit the high 150s/low 160s level.

I am long GS right now, and added on Thursday's decline.

I am long GS right now, and added on Thursday's decline.

I see the decline of GS over the past few weeks, and think it is very over stated. With the bill coming through over the next few weeks, reported earnings coming due and the fact that GS is trading very close to book value, I am expecting GS bounce and hit the high 150s/low 160s level.

I am long GS right now, and added on Thursday's decline.

I am long GS right now, and added on Thursday's decline.

Thursday, June 10, 2010

Market Thought... thinking alike

Apparently my thesis is pretty similar to Bob Doll's (from BlackRock) thesis. (see video) Great minds think alike ;) jk

He sums up a lot of the points, and mentions deflation as his biggest concern to change his thesis. I stated the same in previous 'market thought' posts, deflation was my concern as well. The method I am assessing it, so that I adjust my thesis and portfolio, is if we get a severe breakdown in the 10yr treasury from the 3.0-3.1% levels.

Since a 'really-big' big-boy highlights the same concern, it re-enforces me that I am following the correct market indicator for my thesis.

Since a 'really-big' big-boy highlights the same concern, it re-enforces me that I am following the correct market indicator for my thesis.

The fact that the 10yr bounced off nicely from the 3.2 level was encouraging.

He sums up a lot of the points, and mentions deflation as his biggest concern to change his thesis. I stated the same in previous 'market thought' posts, deflation was my concern as well. The method I am assessing it, so that I adjust my thesis and portfolio, is if we get a severe breakdown in the 10yr treasury from the 3.0-3.1% levels.

Since a 'really-big' big-boy highlights the same concern, it re-enforces me that I am following the correct market indicator for my thesis.

Since a 'really-big' big-boy highlights the same concern, it re-enforces me that I am following the correct market indicator for my thesis.The fact that the 10yr bounced off nicely from the 3.2 level was encouraging.

Twilight Zone

Sometimes you are damned if you do, and damned if you don't. At what point did the average person feel so bad for big sophisticated investors that they directed their anger soooo much toward the broker.

The public anger toward Goldman is nothing more than the average person thinking Goldman did something wrong to them. But that is not the case, not the case at all.

Whatever evils Goldman may have done, one thing is for certain, they did NOTHING to the average investor.

Big banks were dealing with big banks (or hedge funds), and Goldman was in-between. Yet the little guy thinks it is somehow related to them. Its not, no matter how many dots you connect or degree of separation you are looking at. The fact of the mater is Goldman did not dupe stupid unsophisticated investors. They delt with people who are certified to be in this business.

The second people start realizing this fact, they can focus on more important things like properly regulating Fannie and Freddie Mac. Or putting to jail the CEOs that were reckless with their companies, and the financial system.

Watching the public deterioration of a bank that actually did the right thing, with risk management, is disturbing. Its a disturbing moral hazard. Basically the SEC, and public, is saying it was better to fail and cost tax payers money, then institute the correct practice.

Ethically GS may have been wrong, but we can not police ethics, only actions. Nothing is perfect, and ethics can always be improved, but at what point do we say enough-is-enough. At what point are individual certified investors responsible for their own actions.

After all, if the demand for these security products were not present at the time, a credit bubble would not have been formed. Just like when there was no demand for corporate credit in 2008, the economy pretty much stopped for a few months.

The public anger toward Goldman is nothing more than the average person thinking Goldman did something wrong to them. But that is not the case, not the case at all.

Whatever evils Goldman may have done, one thing is for certain, they did NOTHING to the average investor.

Big banks were dealing with big banks (or hedge funds), and Goldman was in-between. Yet the little guy thinks it is somehow related to them. Its not, no matter how many dots you connect or degree of separation you are looking at. The fact of the mater is Goldman did not dupe stupid unsophisticated investors. They delt with people who are certified to be in this business.

The second people start realizing this fact, they can focus on more important things like properly regulating Fannie and Freddie Mac. Or putting to jail the CEOs that were reckless with their companies, and the financial system.

Watching the public deterioration of a bank that actually did the right thing, with risk management, is disturbing. Its a disturbing moral hazard. Basically the SEC, and public, is saying it was better to fail and cost tax payers money, then institute the correct practice.

Ethically GS may have been wrong, but we can not police ethics, only actions. Nothing is perfect, and ethics can always be improved, but at what point do we say enough-is-enough. At what point are individual certified investors responsible for their own actions.

After all, if the demand for these security products were not present at the time, a credit bubble would not have been formed. Just like when there was no demand for corporate credit in 2008, the economy pretty much stopped for a few months.

Wednesday, June 9, 2010

Market Thought... big boys, grow-a-pair

Too many people 'think' they understand the technicals, but are using the wrong support/resistance points.

Here is some sanity. The ultimate level of support for the SP500 is the daily 320 SMA. period. I do not care what other horizontal, triangular or whatever shape/directional support anyone whats to tout, the 320 SMA on the daily SP500 is THE support.

The support many are touting right now is coming from the 62 SMA in the weekly and the 14 and 200 SMAs via the monthly. Hence the importance of the current market level. (But it is being misinterpreted as horizontal support or some other support.)

Here is the interesting part. If the SP500 breaks from this current intra-week/month support, we will see the daily 320SMA. But this is where I feel the computers will be on the long side.

As we breach, any hedgie left in the market (which are few) most likely will get stopped out. (Or at least the ones that feel the 1040-1050 level is important.) But computers do not give a shit. Computers, or the algorithmic trading platforms, follow patterns. While the big-boys are curled in a fetal position, the computers will be buying, and give us a capitulation.

If we breach, I believe it will only be for the intra-week/month, and resume the SP500 weekly/monthly low end support.

Looking at the correct resistance point, today's reversal was no surprise. It bounced off its 14SMA down trend resistance.

Looking at the correct resistance point, today's reversal was no surprise. It bounced off its 14SMA down trend resistance.

FYI... AAPL reached my entry point, via the technicals and I added. If/when we get this capitation I will add to IBM, AAPL and maybe even BP.

Here is some sanity. The ultimate level of support for the SP500 is the daily 320 SMA. period. I do not care what other horizontal, triangular or whatever shape/directional support anyone whats to tout, the 320 SMA on the daily SP500 is THE support.

The support many are touting right now is coming from the 62 SMA in the weekly and the 14 and 200 SMAs via the monthly. Hence the importance of the current market level. (But it is being misinterpreted as horizontal support or some other support.)

Here is the interesting part. If the SP500 breaks from this current intra-week/month support, we will see the daily 320SMA. But this is where I feel the computers will be on the long side.

As we breach, any hedgie left in the market (which are few) most likely will get stopped out. (Or at least the ones that feel the 1040-1050 level is important.) But computers do not give a shit. Computers, or the algorithmic trading platforms, follow patterns. While the big-boys are curled in a fetal position, the computers will be buying, and give us a capitulation.

If we breach, I believe it will only be for the intra-week/month, and resume the SP500 weekly/monthly low end support.

Looking at the correct resistance point, today's reversal was no surprise. It bounced off its 14SMA down trend resistance.

Looking at the correct resistance point, today's reversal was no surprise. It bounced off its 14SMA down trend resistance.FYI... AAPL reached my entry point, via the technicals and I added. If/when we get this capitation I will add to IBM, AAPL and maybe even BP.

Tuesday, June 8, 2010

Gold charts

Below are the charts of Gold via the GLD. The daily indicates the stress from the double top, and the weekly indicates the same but on a longer horizon. The weekly is hovering around the Nov 2009 high, and has yet to break free from it.

Make no mistake, the uptrend is still very much intact, on both charts. But visible resistance is currently at hand.

Make no mistake, the uptrend is still very much intact, on both charts. But visible resistance is currently at hand.

Keep in mind:

I do not like trading GLD, even though I may do it from time to time purely on the technicals, because I can not make sense of the fundamentals. I can not see a trend-shifting stress the way I was able to see with Oil at 140-147. There is just so much more information available to a 'non-insider' commodity trader for the oil market to identify real upward stress. The way I identified the upward stress in oil is by correlating Oil's fundamental disconnect with the stress of its chart. (That spoke volumes to me to take a short trade on. ) I do not see the fundamental side of Gold so I can not truly assess if this is a peak.

Make no mistake, the uptrend is still very much intact, on both charts. But visible resistance is currently at hand.

Make no mistake, the uptrend is still very much intact, on both charts. But visible resistance is currently at hand.Keep in mind:

I do not like trading GLD, even though I may do it from time to time purely on the technicals, because I can not make sense of the fundamentals. I can not see a trend-shifting stress the way I was able to see with Oil at 140-147. There is just so much more information available to a 'non-insider' commodity trader for the oil market to identify real upward stress. The way I identified the upward stress in oil is by correlating Oil's fundamental disconnect with the stress of its chart. (That spoke volumes to me to take a short trade on. ) I do not see the fundamental side of Gold so I can not truly assess if this is a peak.

Monday, June 7, 2010

Market Thought... everyone is right

Because I follow such a board media presence I see a ton, a ton, of polar opposite opinions on the current market and market expectations.

The problem is, no one is stating their caveats. Reading such craziness is taxing, and can destroy one's discipline if reasons behind their estimates are ignored. All projections depend on the 'if/then' scenario that play out. (If Europe does not collapse, equity markets will not collapse. If Europe collapses, then global equity markets collapse.) Its that simple, but analyst state things with such conviction that you have to have a strong basis to your own thesis. On the same breath, we must identify the correct indicator(s) that would suggest the low probability views come to fruition, so a change in position can take place. (Hence my 're-evaluation' post, and my consistent Market Thought posts.)

Now, all I can do is act on my thesis, until I see the breakdown in the 10year treasury yield. So today I added to GS (options), C (common) and my limit order for NAT (common) got executed end-of-day. If the market is weak from here, AAPL may see between 240-245 and IBM may see 122-123, and I will be a buyer of both. Here is why, I think the charts speak for themselves:

The problem is, no one is stating their caveats. Reading such craziness is taxing, and can destroy one's discipline if reasons behind their estimates are ignored. All projections depend on the 'if/then' scenario that play out. (If Europe does not collapse, equity markets will not collapse. If Europe collapses, then global equity markets collapse.) Its that simple, but analyst state things with such conviction that you have to have a strong basis to your own thesis. On the same breath, we must identify the correct indicator(s) that would suggest the low probability views come to fruition, so a change in position can take place. (Hence my 're-evaluation' post, and my consistent Market Thought posts.)

Now, all I can do is act on my thesis, until I see the breakdown in the 10year treasury yield. So today I added to GS (options), C (common) and my limit order for NAT (common) got executed end-of-day. If the market is weak from here, AAPL may see between 240-245 and IBM may see 122-123, and I will be a buyer of both. Here is why, I think the charts speak for themselves:

AAPL and GS

1. AAPL - the new iPhone is just sick. I still find myself being impressed even though I, like every other Apple Fan Boy saw the phone coming. What it can do is just awesome, and miles ahead of the current version.

2. GS - added to the position.

2. GS - added to the position.

Trade - AAPL

I am waiting on the weakness to level off, but I am awfully tempted to step in an buy AAPL calls here.

The reasons:

1. technically, it is at a support level around the low 250s

2. it is freaken cheap. (on an discounted cash flow perspective)

lets look at the number in a dirty and quick manner...

The liquid cash the company has on hand is about $25B, which equates to $25/share. Take the cash value out of the stock at current price (253-25= 228) and we have a stock trading at est. 2010 PE of 17-18. BUT...

The stock has about another $20B in cash, which is considered illiquid (meaning it is tied up for a few months or years). Combine the cash hoard, and we have an equity who's future earnings power is being discounted to an est. 2010 PE of 15. (253-40=213; 213/13.80 = 15.4)

AAPL's large market cap is already being discounted in its valuation. (Do not believe the analyst that tell you other wise.) If you look at the future earnings of this company going out 2-3yrs, its EPS will continue to grow at a +15-20% clip. The 2010 est. PE (excluding cash) is telling investors that AAPL will grow EPS at less than 15% going forward.

Does that sound realistic?

(Heaven for bid something happens to Steve Jobs sometime in the near future, the earnings power of this company will be greater than 15% eps for the next few years.)

The reasons:

1. technically, it is at a support level around the low 250s

2. it is freaken cheap. (on an discounted cash flow perspective)

lets look at the number in a dirty and quick manner...

The liquid cash the company has on hand is about $25B, which equates to $25/share. Take the cash value out of the stock at current price (253-25= 228) and we have a stock trading at est. 2010 PE of 17-18. BUT...

The stock has about another $20B in cash, which is considered illiquid (meaning it is tied up for a few months or years). Combine the cash hoard, and we have an equity who's future earnings power is being discounted to an est. 2010 PE of 15. (253-40=213; 213/13.80 = 15.4)

AAPL's large market cap is already being discounted in its valuation. (Do not believe the analyst that tell you other wise.) If you look at the future earnings of this company going out 2-3yrs, its EPS will continue to grow at a +15-20% clip. The 2010 est. PE (excluding cash) is telling investors that AAPL will grow EPS at less than 15% going forward.

Does that sound realistic?

(Heaven for bid something happens to Steve Jobs sometime in the near future, the earnings power of this company will be greater than 15% eps for the next few years.)

Gonna be interesting...

If the pre-market is a gauge to Monday's trading, looks like it will be interesting. Regardless, all of Wall Street was preparing for a horrible week (this week). Last I checked the SP500 futures were down about 9 points, and this should correlate to GS being down nicely too. The reason I highlight GS is because on Friday, Guy Adami (of Fast Money) brought to light GS' book value.

A quick look on Yahoo Finance reveals GS has a book value of 128.33. Analysts can argue until they are blue in the face regarding how a banks value their assets, but the one thing I do know is that GS has a very long history valuing its own assets extremely conservatively. So the 128 level is fairly legitimate.

GS currently trades at 142. With the sizable market decline expected, intraday action could lead GS to the high 130s. If this happens, I will be a buyer of GS.

A quick look on Yahoo Finance reveals GS has a book value of 128.33. Analysts can argue until they are blue in the face regarding how a banks value their assets, but the one thing I do know is that GS has a very long history valuing its own assets extremely conservatively. So the 128 level is fairly legitimate.

GS currently trades at 142. With the sizable market decline expected, intraday action could lead GS to the high 130s. If this happens, I will be a buyer of GS.

Saturday, June 5, 2010

Market Thought... re-evaluation

The technicals of the market continue to look horrible, and frankly I do not think they matter at the moment. The one indicator I am keen on is the 10yr treasury. The yield is about to retest a level (3.0-3.1%) that (if severely broken) may signal deflation, which would relate to a weak equities market.

The piss-poor Jobs Report was so bad, it made me take a long-hard look at my bullish market thesis. Since Friday morning I have been thinking, reading and contacting people that can help me piece the puzzle together.

1. Jobs:

The private jobs growth of 41K was piss poor. On Friday I contacted some Head Hunter friends of mine, and what they are seeing does not corroborate with the Jobs Report.

-One firm is seeing record numbers, and a sense of stress with companies looking too specifically for criteria regarding talent. It appears a tipping point is being achieved where 'good-enough' talent have to fill a company's desired role.

-June was also considered a busy month, but July and August are generally slow. Then a drastic pick up in Sept. (This next report maybe more reflective of what the Hunters were seeing.)

Obviously this is very qualitative, and not scientific by any means. (If I had the time and resources to contact over 20 or so ground level Head Hunters or a few executives I could produce a more quantitative model of expectations. The only quantitative model I have regarding full time employment expectations is MWW stock. One can assume if the private jobs market is good, the trading habits of a forward looking stock would indicate this. But right now the stock is not indicating the qualitative findings.

One thing that can corroborate the qualitative findings is the high productivity rate for corporate America. My discussions indicate to me, the level is unsustainable, and a point for optimism.

2. Corporate Profits:

The market is driven by profits, or expectations of profits, (everything else is essentially noise that people assume will affect profits) and the 'Hours and Earnings of all Employees' still increased, and it has consistently increased since last year.

This current Jobs report is the only one that would lead to the lack of sustainability toward Employment Earnings. With so much public sector job increases, it is hard to argue otherwise. But there is still a lot of stimulus money not spent yet, along with the gradual reduction in productivity level from job growth, corporate profits should remain high for the rest of 2010. (And with the global economy growing, companies positioned for the growth will continue to grow profits.)

3. Europe (from banks-to-politics)

I still believe there is a 'perceived negativity' in Europe that is acting as a domino effect. The risk of default or breaking of the Euro is squashed. Austerity measures are being passed across the continent, and countries that need help are being dragged kicking and screaming via the IMF. In my opinion, this risk is being reduced. However, a domino effect of the default is jump-starting rumors regarding high profile bank failures, along with derivative losses from others. The ECB apparently has been on this, and is taking action. (article) With their own stress tests established, this may alleviate this domino-effect. (I also think a awesome buying opportunity will be established for STD when or if a secondary is required from the stress test. I will be looking to buy STD if a secondary is announced.)

Also, the decline in the Euro does not worry me. The rate of decline is a concern, but this will begin to mitigate itself (as the markets find an equilibrium) to present a new carry trade the Hedgies can exploit. (Just like they did with the dollar/yen for years.) I find it hard to believe anyone was not expecting the Euro to decline once the Greece situation was first mentioned in the early parts of the year.

4. China Slowing:

The Chinese have proven time and time again that they have too much control over their economy. I mean some of the numbers that come out of China w/respect to bank lending can swing wildly, and make me scratch my head. We can see consumers borrow north of $190b in one month, then borrow close to nothing the next month. Also, their government has too much money to let their 'economic miracle' simply dwindle now. Over the last 20 years they (the controllers of their economy) have shown to have too much control, and I do not think they will loose it just yet. (But I do think commodities continue to under-perform due to their direct involvement in China slowing down their real-estate construction boom. That is just common sense.)

Fact of the matter...

The cold truth is that the US and global economy can be sustained and grow with a higher unemployment number. Corporate profits are growing. Political leaders are doing what they have to do to maintain stability, even though sometimes we cringe at what they do.

The austerity measure will hurt some, the unemployment rate will hurt some, but those 'some' just do not matter with respect to the economy.

(Although the above statement seems arrogant, keep in mind, I will be one of those 'some' in a few months as I will be laid-off due to Pfizer's closure of a vaccine manufacturing site. I do not make that statement lightly. My knees and knuckles are too bloody from trying to continuously better myself, and my family's, well being to carelessly make that statement. It is merely a point of fact.)

The piss-poor Jobs Report was so bad, it made me take a long-hard look at my bullish market thesis. Since Friday morning I have been thinking, reading and contacting people that can help me piece the puzzle together.

1. Jobs:

The private jobs growth of 41K was piss poor. On Friday I contacted some Head Hunter friends of mine, and what they are seeing does not corroborate with the Jobs Report.

-One firm is seeing record numbers, and a sense of stress with companies looking too specifically for criteria regarding talent. It appears a tipping point is being achieved where 'good-enough' talent have to fill a company's desired role.

-June was also considered a busy month, but July and August are generally slow. Then a drastic pick up in Sept. (This next report maybe more reflective of what the Hunters were seeing.)

Obviously this is very qualitative, and not scientific by any means. (If I had the time and resources to contact over 20 or so ground level Head Hunters or a few executives I could produce a more quantitative model of expectations. The only quantitative model I have regarding full time employment expectations is MWW stock. One can assume if the private jobs market is good, the trading habits of a forward looking stock would indicate this. But right now the stock is not indicating the qualitative findings.

One thing that can corroborate the qualitative findings is the high productivity rate for corporate America. My discussions indicate to me, the level is unsustainable, and a point for optimism.

2. Corporate Profits:

The market is driven by profits, or expectations of profits, (everything else is essentially noise that people assume will affect profits) and the 'Hours and Earnings of all Employees' still increased, and it has consistently increased since last year.

This current Jobs report is the only one that would lead to the lack of sustainability toward Employment Earnings. With so much public sector job increases, it is hard to argue otherwise. But there is still a lot of stimulus money not spent yet, along with the gradual reduction in productivity level from job growth, corporate profits should remain high for the rest of 2010. (And with the global economy growing, companies positioned for the growth will continue to grow profits.)

3. Europe (from banks-to-politics)

I still believe there is a 'perceived negativity' in Europe that is acting as a domino effect. The risk of default or breaking of the Euro is squashed. Austerity measures are being passed across the continent, and countries that need help are being dragged kicking and screaming via the IMF. In my opinion, this risk is being reduced. However, a domino effect of the default is jump-starting rumors regarding high profile bank failures, along with derivative losses from others. The ECB apparently has been on this, and is taking action. (article) With their own stress tests established, this may alleviate this domino-effect. (I also think a awesome buying opportunity will be established for STD when or if a secondary is required from the stress test. I will be looking to buy STD if a secondary is announced.)

Also, the decline in the Euro does not worry me. The rate of decline is a concern, but this will begin to mitigate itself (as the markets find an equilibrium) to present a new carry trade the Hedgies can exploit. (Just like they did with the dollar/yen for years.) I find it hard to believe anyone was not expecting the Euro to decline once the Greece situation was first mentioned in the early parts of the year.

4. China Slowing:

The Chinese have proven time and time again that they have too much control over their economy. I mean some of the numbers that come out of China w/respect to bank lending can swing wildly, and make me scratch my head. We can see consumers borrow north of $190b in one month, then borrow close to nothing the next month. Also, their government has too much money to let their 'economic miracle' simply dwindle now. Over the last 20 years they (the controllers of their economy) have shown to have too much control, and I do not think they will loose it just yet. (But I do think commodities continue to under-perform due to their direct involvement in China slowing down their real-estate construction boom. That is just common sense.)

Fact of the matter...

The cold truth is that the US and global economy can be sustained and grow with a higher unemployment number. Corporate profits are growing. Political leaders are doing what they have to do to maintain stability, even though sometimes we cringe at what they do.

The austerity measure will hurt some, the unemployment rate will hurt some, but those 'some' just do not matter with respect to the economy.

(Although the above statement seems arrogant, keep in mind, I will be one of those 'some' in a few months as I will be laid-off due to Pfizer's closure of a vaccine manufacturing site. I do not make that statement lightly. My knees and knuckles are too bloody from trying to continuously better myself, and my family's, well being to carelessly make that statement. It is merely a point of fact.)

Friday, June 4, 2010

Jobs Report... piss poor

The report was piss poor. I did not care for the head line number, but was looking primarily at the private sector job growth of 41k. There is nothing to be happy about in it. Linked is the break down from bls.gov (table). Market has every reason to sell of today, every reason.

Still looking to enter the names posted yesterday with this decline. My target prices will be for the low end, as this jobs report may force the SP500 to test the low end of its range again (over the next week or so).

Still looking to enter the names posted yesterday with this decline. My target prices will be for the low end, as this jobs report may force the SP500 to test the low end of its range again (over the next week or so).

Thursday, June 3, 2010

Potential Trades - GS, AAPL, CHK

GS - If GS approaches its 14SMA (around 141) I will add to it. I am already in it, but the current activity around 145 has consolidated the name from its very-short-term overbought position.

CHK - Based on the previous chart I highlighted the other day, the target of 18 may not be viable. President Obama's talk of Nat.Gas (along with Cramer's highlight of it) changed the trading dynamic of the stock. A more realistic target, based on its new trading dynamic, would be around 20.

AAPL - I would rather wait for it to fall between 250-255, but it is close to its 5 SMA (which acts as support when it is in a momentum move).

Tuesday, June 1, 2010

Market Thought... butter

My word for the rest of 2010 will be 'butter'.

The markets are churning so much, it is as if the markets are making the stuff. Then, when the fear fades and the markets rally, the markets will be butter. (look up butter on urbandictionary.com for those who do not get the slang ;)

I am not backing away from the thesis of the recent Market Thought post 'resistance?'. The markets are playing out the very uncertainty highlighted, and its churning. This has to play out until things look better, and if the economic data holds up, it will play out.

I have made no secret that with this market churning, when the SP500 meets the daily 320SMA (which can be around 1040/1050, not the current SMA level), I will go very heavy into this market. I will be adding to my usual suspects (ie IBM, AAPL, GS, NAT, F, KMP, C and maybe GOOG among others).

A few stocks I am really interested in with this market decline include ERII and CHK. Most of my capital I plan on allocating to the names above, but with the oil spill, Shell's recent announcement of a Nat.Gas. acquisition and Nat.Gas prices holding steady CHK is very appealing. If I can get CHK for around 18, I will not pass it up.

ERII, to me, is one of the best pure play water themes (along with NLC). I wish management would execute a better acquisition strategy to flatten out their extremely bumpy earnings. (They have to define to Wall Street what kind of company they have to become. There current product line up, while technologically impressive is not cutting it for investors.) Regardless, it is approaching levels that a deep value player can not ignore. Their product(s) are proven, in demand and the company is legit. Asset Valuation (excluding intangibles and goodwill) its worth in the mid/high 2s. Book Value its worth in the high 1s. And Cash Value alone its worth about 1 dollar a share. If ERII enters the mid/high 2s, I will buy a few thousand shares on shear valuation alone. (But I warn, the chart is not pretty, indicating a strong and consistent liquidation going on right now.)

The markets are churning so much, it is as if the markets are making the stuff. Then, when the fear fades and the markets rally, the markets will be butter. (look up butter on urbandictionary.com for those who do not get the slang ;)

I am not backing away from the thesis of the recent Market Thought post 'resistance?'. The markets are playing out the very uncertainty highlighted, and its churning. This has to play out until things look better, and if the economic data holds up, it will play out.

I have made no secret that with this market churning, when the SP500 meets the daily 320SMA (which can be around 1040/1050, not the current SMA level), I will go very heavy into this market. I will be adding to my usual suspects (ie IBM, AAPL, GS, NAT, F, KMP, C and maybe GOOG among others).

A few stocks I am really interested in with this market decline include ERII and CHK. Most of my capital I plan on allocating to the names above, but with the oil spill, Shell's recent announcement of a Nat.Gas. acquisition and Nat.Gas prices holding steady CHK is very appealing. If I can get CHK for around 18, I will not pass it up.

ERII, to me, is one of the best pure play water themes (along with NLC). I wish management would execute a better acquisition strategy to flatten out their extremely bumpy earnings. (They have to define to Wall Street what kind of company they have to become. There current product line up, while technologically impressive is not cutting it for investors.) Regardless, it is approaching levels that a deep value player can not ignore. Their product(s) are proven, in demand and the company is legit. Asset Valuation (excluding intangibles and goodwill) its worth in the mid/high 2s. Book Value its worth in the high 1s. And Cash Value alone its worth about 1 dollar a share. If ERII enters the mid/high 2s, I will buy a few thousand shares on shear valuation alone. (But I warn, the chart is not pretty, indicating a strong and consistent liquidation going on right now.)

Subscribe to:

Posts (Atom)