So, Google+ designers were Apple guys. Now Google is using Guy Kawasaki to facilitate hardware.

Is there any real doubt Google wants to be more Apple-like?

Thursday, February 28, 2013

Why does $GOOG have a PE near 25?

I can answer the question with solid arguments (ultimately I'm a Google bull), but I still do not understand why Google's size is getting a free pass.

1. Google has a market capitalization of $260 BILLION.

When Apple was a $260B market cap, it was growing earnings around a +85% rate, and its trailing multiple did not go above 25. In fact, it never saw a PE of 25 again. Despite a HUGE, absolutely huge, growth rate.

In fact, the only time I recall very large market cap. companies having such a high trailing multiple was during the tech bubble.

2. Google's core business, search, of which still earns Google +90% of its earnings, has peak market share. Desktop share has been hovering around 65-67% for a while now. Mobile share has been in the high 90% ever since Apple created the 'post-pc' world.

Google can not rely on outpacing the sector, when its market share has peaked. It must rely on sector growth. Is the mobile Ad space going to grow at a rate justifying a high multiple for a very large company. (And while mobile will grow, it will disrupt desktop. So there will be a push-pull growth relationship it will have to combat.)

3. Google's new line of businesses. Hardware. Looks like Google want to get into the premium hardware space with Google Glasses and Chrome Pixel. And if that is the case, then a shift to self branding of their Nexus devices is on the way.

Would the expected growth from hardware driving higher street expectations, allowing for a high multiple for such a large company? The very fickle business line that causes a constant poo-pooing of Apple from the hardcore droid-boys or Apple-bears.

So, how is the 3rd largest US corporation going to justify a trailing multiple near 25? (P.S. none of the largest 20 US corporations have a trailing multiple greater that 20.)

I simply do not know.

From the looks of how Google is transitioning, Google is building a consumer hardware business from its web-services. Seemingly copying Apple along the way. As if they want to be viewed as the "new Apple". The only problem, Apple is Apple.

Wednesday, February 27, 2013

$vz is losing it

They have to step up their LTE game in the east coast. For a few weeks now it has been crappy. It was pretty good, but became inconsistent and crappy. Now their 3G is barely working.

AT&T LTE is giving better reliability. (Its noticeably faster too.)

AT&T LTE is giving better reliability. (Its noticeably faster too.)

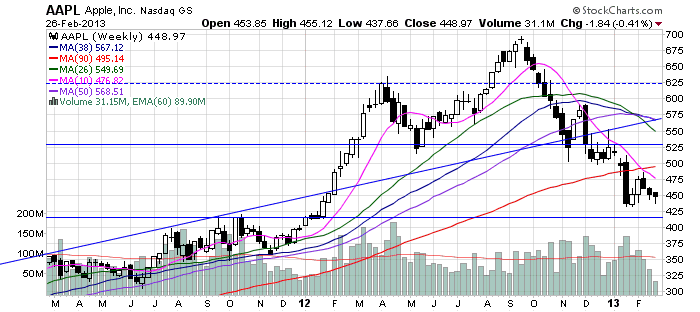

Tuesday, February 26, 2013

Nice intra day... $aapl

I really want to get excited about AAPL right here.

Some nice intra day activity. If it holds, the action could confirm the bottom, and at the very least, start the process of forming a head and shoulders on the weekly chart.

This means the stock could be on its way to test the high 500s/low 600s. (Will post charts later.)

PS: seeing a report that Doug Kass sparked the reversal w/ a stock split tweet. The timing makes sense, but a split doesn't cause a stock to rally.

updated:

The intra day action saw a clear high value spike around 1:30 - 1:50pm

Some nice intra day activity. If it holds, the action could confirm the bottom, and at the very least, start the process of forming a head and shoulders on the weekly chart.

This means the stock could be on its way to test the high 500s/low 600s. (Will post charts later.)

PS: seeing a report that Doug Kass sparked the reversal w/ a stock split tweet. The timing makes sense, but a split doesn't cause a stock to rally.

updated:

The intra day action saw a clear high value spike around 1:30 - 1:50pm

That break upward facilitated a firming up of the daily chart via a higher-low rounding bottom.

If solid footing among the stock can maintain itself, there is a slew of obvious resistance markers on the weekly via the SMAs. The first level of resistance points are the 10SMA, and the low 500 (pre-Q1 earnings level). When sentiment shift, a simply shift that would facilitate the stock to be trading with a decent multiple, near 12-13, a the head-and-sholder pattern will emerge.

Market Thought... "Berlusconi-ed"

Now the world knows how it feels like to be an underaged girl at a bunga-bunga party.

The markets got Berlusconi-ed.

Regardless of the fondling of the bunga-bunga, the markets were also due for a pull back.

Barring a credit-event coming out of China, and the US employment data stays healthy, the markets should be okay. Given the Google Trends on 'jobless claims', the US seems to be okay.

While the markets are consolidating, some interesting trades are developing.

AET - looking for a bounce off the 68SMA.

DIS - looking for a test of the 62SMA.

The markets got Berlusconi-ed.

Regardless of the fondling of the bunga-bunga, the markets were also due for a pull back.

Given the magnitude of the Vix spike, the SP500 should find support soon. An argument for strong support can be made between 1450-1470 via the daily, weekly and monthly charts.

The one good thing that came out of the Berlusconi-cluster-fuck could be a lower Euro, which should help the EU economy.

While the markets are consolidating, some interesting trades are developing.

AET - looking for a bounce off the 68SMA.

DIS - looking for a test of the 62SMA.

eBAY - looking for the 90SMA to be tested.

Thursday, February 21, 2013

Law of large numbers don't matter anymore? $goog

Google upgraded with a $1000 price.

I'm a fan of google, but do the laws of large numbers no longer apply for Google?

For a company with maximum market share on the desktop and mobile platforms, is the overall ad market going to grow quick enough to justify a trailing multiple of 25 for a company with a +$260B market cap? (Is the market expecting AAPL like growth? Because the market is ignoring Apple's Apple-like growth.)

I'm a fan of google, but do the laws of large numbers no longer apply for Google?

For a company with maximum market share on the desktop and mobile platforms, is the overall ad market going to grow quick enough to justify a trailing multiple of 25 for a company with a +$260B market cap? (Is the market expecting AAPL like growth? Because the market is ignoring Apple's Apple-like growth.)

Market Thought... China and the Fed

The market was crappy pretty much all day, but it really started to kick downward after the Fed minutes were released.

Looks like China may have led the US.

I would like to think the SP500 sees a healthy 3% (or so) pull back toward 1450-1460 area, but I am not convinced that will happen just yet.

Taking a cue from market leaders, despite today's decline, they are structurally sound from their high-momentum short-term SMAs. I'm looking for the stocks to start cracking the SMAs to see a real pull back. GOOG, GS and VLO are examples.

Looks like China may have led the US.

I would like to think the SP500 sees a healthy 3% (or so) pull back toward 1450-1460 area, but I am not convinced that will happen just yet.

Taking a cue from market leaders, despite today's decline, they are structurally sound from their high-momentum short-term SMAs. I'm looking for the stocks to start cracking the SMAs to see a real pull back. GOOG, GS and VLO are examples.

Wednesday, February 20, 2013

hit job vs data... $aapl

1. iPhone 5 and 4S outsells the Galaxy 3S by over 2:1 in Q4 via Strategy Analytics. But for an Apples-to-Apples comparison, the 4S (alone) still out sold the Galaxy 3S.

2. The FT is out with a report that Foxconn slow hiring due to the slow down of the iPhone. (Almost too predictable, as AAPL is testing its SMA support. Smells like another WSJ-like hit job.)

The futures say the hit-job wins. Fucking annoying.

Looking for AAPL to settle above 440. If it can do that, this new hit-job will not do structural damage to the bottoming process.

2. The FT is out with a report that Foxconn slow hiring due to the slow down of the iPhone. (Almost too predictable, as AAPL is testing its SMA support. Smells like another WSJ-like hit job.)

The futures say the hit-job wins. Fucking annoying.

Looking for AAPL to settle above 440. If it can do that, this new hit-job will not do structural damage to the bottoming process.

Monday, February 18, 2013

will $amzn be next?

While Apple was not the first tech-centric company to have a retail store, the stores are powerful. (In terms of revenue/earnings, costumer satisfaction and connecting with the local community.)

The success had Microsoft follow. Now, Google is looking to get in the retail game. I am not a fan of blind speculation, but how Google approaches retail can be good or can be very messy.

Will the retail outlets leverage all (or select) the Android OEMs or focus solely on the Nexus brands (or whatever is considered "Google hardware")? The former implies an inventory mess, along with potentially pissing-off OEMs if they somehow feel excluded, pushing them deeper into Windows 8. The latter implies an Apple-like store to make the Nexus brand a house hold name. Allowing Google to sell the Nexus brands for profit. (Or selling the hardware for a somewhat higher price or for greater margins as the locations have to be funded.)

If Apple, Microsoft and Google have a retail presence, will Amazon follow suit to facilitate their Kindle line?

If Amazon truly wants to get a critical mass with their tablets, Apple proved retail locations work. But Bezos knows Wall Street too well. Retail stores for Amazon removes the promise of Amazon: A dominant invisible retailer that does not have the over-head of brick-and-mortar. Retail stores will allow analysts to compare to other retailers. Retail sales will allow for a level of transparency regarding tablet sales. This transparency is a threat to Amazon. Transparency will justifying a lower valuation.

The success had Microsoft follow. Now, Google is looking to get in the retail game. I am not a fan of blind speculation, but how Google approaches retail can be good or can be very messy.

Will the retail outlets leverage all (or select) the Android OEMs or focus solely on the Nexus brands (or whatever is considered "Google hardware")? The former implies an inventory mess, along with potentially pissing-off OEMs if they somehow feel excluded, pushing them deeper into Windows 8. The latter implies an Apple-like store to make the Nexus brand a house hold name. Allowing Google to sell the Nexus brands for profit. (Or selling the hardware for a somewhat higher price or for greater margins as the locations have to be funded.)

If Apple, Microsoft and Google have a retail presence, will Amazon follow suit to facilitate their Kindle line?

If Amazon truly wants to get a critical mass with their tablets, Apple proved retail locations work. But Bezos knows Wall Street too well. Retail stores for Amazon removes the promise of Amazon: A dominant invisible retailer that does not have the over-head of brick-and-mortar. Retail stores will allow analysts to compare to other retailers. Retail sales will allow for a level of transparency regarding tablet sales. This transparency is a threat to Amazon. Transparency will justifying a lower valuation.

Wednesday, February 13, 2013

Smartphone Growth... $aapl $goog $qcom

Gartner 2012 global mobile sales numbers are out:

-total units 1.75billion units

-total smartphones 207.7million units

-smartphone penetration 11.9%

Plenty of room for growth in the smartphone sector.

-total units 1.75billion units

-total smartphones 207.7million units

-smartphone penetration 11.9%

Plenty of room for growth in the smartphone sector.

$aapl chart

After listening to Cook today, I got the same feeling I felt when listening to Jamie Dimon when JPM had their 'whale fiasco'. I felt re-assured. Even though the stock is in the shitter, Cook is still one of my favorite CEOs.

Today's decline seems more of a technical selling vs what was said at the conference. AAPL saw technical resistance.

The push back will most likely see the 14SMA. If the stock can consolidate with the SMA, it will signal a set of 'higher-lows'. The set up could lead to a firming of the stock. (This set up was displayed in Dec/Jan but the WSJ article about production cuts derailed the set up. Then the negativity was superimposed by the harsh reaction to earnings.)

Over the past two months, I've been hot/cold trading AAPL. (The nail in the coffin was the reaction to earnings.) Its hard to tell if another fluff piece from the WSJ (or from where ever) will cause the stock to crash through the SMAs or lower supports. (Although I have noticed a shift in tone w/the chatter. Seems like a negative chatter is balanced by positive chatter. Maybe Apple is going on a stealth offensive via the rumors.)

Side note: Not that fundamentals matter anymore, but if there really is any doubt about the power of the iPhone, and its staying power, even with the newer +4.0 Android systems, look East. iPhone tops in Japan. Softbank is doing very well, in large part, due to the iPhone against the larger competitor Domoco. A similar situation is brewing in China, when looking at 3G user data.

(But I have to stop writing about the fundamentals of the iPhone, iPad and their very healthy re-occurring iTunes business because I will only keep convincing myself that their multiple needs to be 13-14 not 10!)

Today's decline seems more of a technical selling vs what was said at the conference. AAPL saw technical resistance.

The push back will most likely see the 14SMA. If the stock can consolidate with the SMA, it will signal a set of 'higher-lows'. The set up could lead to a firming of the stock. (This set up was displayed in Dec/Jan but the WSJ article about production cuts derailed the set up. Then the negativity was superimposed by the harsh reaction to earnings.)

Over the past two months, I've been hot/cold trading AAPL. (The nail in the coffin was the reaction to earnings.) Its hard to tell if another fluff piece from the WSJ (or from where ever) will cause the stock to crash through the SMAs or lower supports. (Although I have noticed a shift in tone w/the chatter. Seems like a negative chatter is balanced by positive chatter. Maybe Apple is going on a stealth offensive via the rumors.)

Side note: Not that fundamentals matter anymore, but if there really is any doubt about the power of the iPhone, and its staying power, even with the newer +4.0 Android systems, look East. iPhone tops in Japan. Softbank is doing very well, in large part, due to the iPhone against the larger competitor Domoco. A similar situation is brewing in China, when looking at 3G user data.

(But I have to stop writing about the fundamentals of the iPhone, iPad and their very healthy re-occurring iTunes business because I will only keep convincing myself that their multiple needs to be 13-14 not 10!)

Tuesday, February 12, 2013

Sounds like a infrastructure commercial

The president is really pushing renewables, infrastructure and manufacturing.

Sunday, February 10, 2013

trades... $BAC $FB

BAC - technical set up is an interesting one:

Considering BAC sat out of Friday's rally, the probability is high that it will chill around mid-11, until it is ready to break-out.

The mid-11 supports maybe breached, but for this to happen I am inclined to think market weakness would cause the breach. BAC can see its 62SMA (low-11/high-10).

FB - Looks like FB would like to trade near mid/low 27. If the 62SMA breaks, it can see 25.

The mid-11 supports maybe breached, but for this to happen I am inclined to think market weakness would cause the breach. BAC can see its 62SMA (low-11/high-10).

FB - Looks like FB would like to trade near mid/low 27. If the 62SMA breaks, it can see 25.

Thursday, February 7, 2013

Wednesday, February 6, 2013

Monday, February 4, 2013

Market Thought... euro'd

Friday's employment situation was not that good, and I was surprised to see the market react with such strength. (The brightest spot was the average weekly earnings continues to rise.) It was not strong enough to kick the 10yr out of its resistance, which capped the market near its monthly resistance.

Many pundits suggested the fuel was from money flows from the 1st of the month. Whether this was true or not, it seemed like the market was going to climb the wall of worry. That is until the weekend.

Over the weekend the markets got "Berlusconi-ed". (I'd like to think the act of being "Berlusconi-ed" is to undo a peaceful multi-year Pan-Euro transition from unproductive-to-productive societies.)

1. In a bid to get re-elected, Berlusconi reverted back to the BS politics and fiscally damaging politics that brought Europe down, by vowed to undo a property tax.

2. Corruption allegation in Spain, threatening to oust the party driving the reform.

Today, the markets reacted.

If the SP500 starts to break its 14 SMA, factoring in the new found EU uneasiness (not a complete uncertainty, or not nearly as bad as the sentiment was prior to ECB action), and weaker US jobs number, the SP500 could test 1450-1460.

Subscribe to:

Posts (Atom)